AUG 2026 Explaining Medicare IRMAA: Why Some Retirees Pay More for Medicare

8/1/2026

Medicare can already feel confusing, and then a letter arrives saying your premium is going up because of something called IRMAA. For many people, this notice is unexpected, frustrating, and unclear.

IRMAA stands for Income-Related Monthly Adjustment Amount. It is an extra amount some Medicare beneficiaries pay for Medicare Part B and Part D if their income is above certain limits.

The good news is that IRMAA does not apply to everyone. In fact, most people with Medicare do not pay it. But for those who do, understanding how it works can help prevent surprises and may even help you challenge or reduce the amount if your financial situation has changed.

What Is Medicare IRMAA?

IRMAA is an additional monthly charge added to your Medicare premium when your income is above a set threshold.

It can apply to:

- Medicare Part B, which covers doctor visits, outpatient care, preventive services, and other medical services

- Medicare Part D, which covers prescription drugs

IRMAA is not based on your current monthly budget or how much you use Medicare. It is based on your income as reported to the IRS.

How Medicare Decides If You Owe IRMAA

Medicare looks at your Modified Adjusted Gross Income, often called MAGI. For IRMAA purposes, MAGI generally means your adjusted gross income plus tax-exempt interest.

There is one important detail that surprises many people: Medicare usually uses tax information from two years ago.

For example, your 2026 Medicare premium may be based on your 2024 tax return. That means someone who recently retired, sold a home, received a large one-time payment, or had unusually high investment income may receive an IRMAA notice even if their income has since gone down.

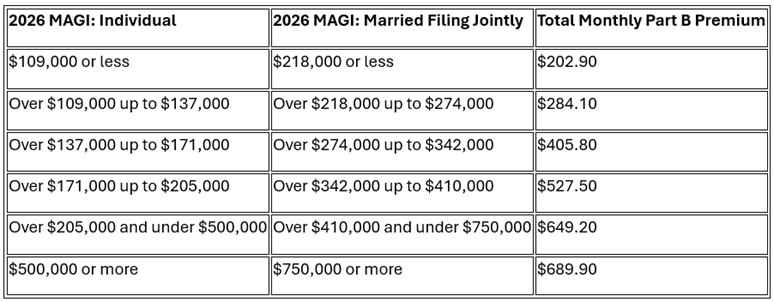

2026 IRMAA Income Levels

For 2026, the standard Medicare Part B premium is $202.90 per month. IRMAA begins when income is above $109,000 for an individual tax filer or above $218,000 for a married couple filing jointly.

Here is a simplified look at the 2026 Part B IRMAA levels:

There is also a separate IRMAA amount for Part D prescription drug coverage. This is added on top of your Part D plan premium. For 2026, the additional Part D IRMAA ranges from $14.50 to $91.00 per month, depending on income.

Why Someone Might Receive an IRMAA Notice

An IRMAA notice can happen for several reasons, including:

- Retirement after a higher-income working year

- Reduced work hours

- A spouse’s death

- Divorce

- A one-time capital gain

- Sale of property or investments

- Required minimum distributions from retirement accounts

- Pension income

- Tax-exempt interest income

- A large bonus, severance payment, or settlement

Sometimes IRMAA is accurate. Other times, it is based on old income that no longer reflects the person’s current financial situation.

Can IRMAA Be Reduced?

Yes, in some cases. If your income has gone down because of a qualifying life-changing event, you may be able to ask Social Security to lower or remove IRMAA.

Common qualifying events include:

- Marriage

- Divorce or annulment

- Death of a spouse

- Work stoppage, such as retirement

- Work reduction

- Loss of income-producing property due to circumstances beyond your control

- Loss of pension income

- Certain employer settlement payments

To request a change, you can use Social Security Form SSA-44, Medicare Income-Related Monthly Adjustment Amount, Life-Changing Event.

You will generally need to provide documentation of the life-changing event and proof of your new or lower income. This may include a signed tax return, tax transcript, employer letter, death certificate, or other supporting records.

What If the Income Was a One-Time Event?

This is where IRMAA can feel especially frustrating. A one-time financial event can push income above the threshold, even if it does not reflect someone’s normal retirement income.

For example, someone may receive IRMAA because they sold an investment, converted part of a traditional IRA to a Roth IRA, sold a home, or received a large severance payment.

Not every one-time income event qualifies for an IRMAA reduction. But if the higher income was connected to a qualifying life-changing event, such as retirement or reduced work, it may be worth contacting Social Security to ask whether a review is possible.

How to Respond to an IRMAA Notice

If you receive an IRMAA notice, do not ignore it. Take the time to review it carefully.

Start by checking:

- Which tax year Social Security used

- Your filing status

- Your modified adjusted gross income

- Whether your income has since gone down

- Whether you had a qualifying life-changing event

- Whether your tax return was later amended

If the information is correct and your income has not changed, the IRMAA amount may apply for the year. If the information is outdated or your circumstances changed, you may have options.

Planning Ahead May Help

IRMAA is one reason retirement tax planning matters. Some financial decisions that seem helpful in one year can increase Medicare premiums two years later.

Before making major financial moves, it may be helpful to talk with a qualified tax professional or financial advisor about how they could affect Medicare premiums. This is especially true for Roth conversions, large investment sales, retirement account withdrawals, and decisions around when to begin drawing income.

The Bottom Line

IRMAA is an extra Medicare cost that applies to higher-income beneficiaries, but it is not always permanent and it is not always based on your current income.

If you receive an IRMAA notice, review it carefully. If your income has dropped because of retirement, reduced work, the death of a spouse, divorce, or another qualifying life event, you may be able to request a new determination.

Understanding IRMAA can help you avoid surprises, protect your monthly budget, and make more informed decisions in retirement.

If Medicare premiums, medical bills, credit card debt, or other expenses are making it difficult to manage your budget, nonprofit credit counseling can help you review your full financial picture and create a plan that works for your situation.

Lori Stratford is the Digital Marketing Manager at Navicore Solutions. She promotes the reach of Navicore's financial education to the public through social media and blog content.

You can follow Navicore Solutions on Facebook, X, LinkedIn and Pinterest. We'd love to connect with you.